The Australian Competition and Consumer Commission’s retail deposit inquiry will pay particular attention to the interest rate structures of deposit products like bonus saver accounts and the extent to which customers actually receive the conditional rates offered on many of these products.

In February, the Treasurer directed the ACCC to conduct an inquiry into the market for retail deposit products supplied by authorised deposit-taking institutions, with a particular focus on how rates are set and the extent of competition.

The ACCC released an issues paper on Friday, setting out the matters it will consider in the inquiry.

It said: “For some accounts that have a base rate and conditional bonus rate, we have only seen the conditional bonus rates increase with movements in the cash rate.

“This means there are potentially a large cohort of consumers who have not seen increases in the cash rate flow through to the interest they receive on their savings.”

The ACCC said that since the RBA started raising the cash rate in May last year, the increases have generally been passed through to interest rates on variable rate home loans. But “the interest rate increases for retail deposit products have often been smaller and conditional”.

Between February 2020 and January 2022, during the COVID lockdown period, aggregate deposits of Australian households rose more than 25 per cent from A$988 billion to $1.2 trillion.

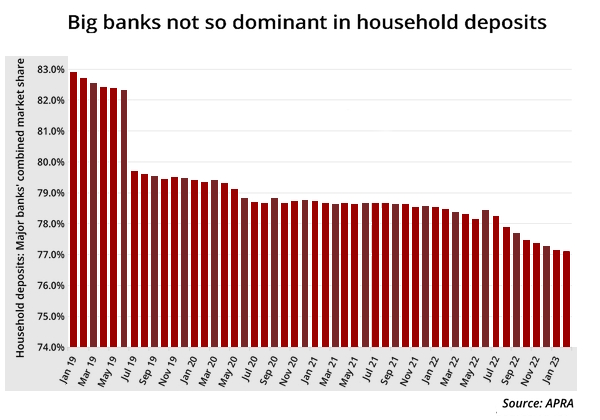

The current aggregate household deposit balance is $1.35 trillion, with the big four banks holding around 73 per cent.

The ACCC said the build-up of deposits during the pandemic may have, to some extent, reduced the competitive pressure for banks to raise deposit interest rates.

It said competition between ADIs for retail deposits is essential for ensuring that consumers are able to achieve positive outcomes in terms of product quality, choice and value.

“Competition is also essential for ensuring the sustainability, strength and resilience of ADIs by incentivising efficient operations and responsiveness to consumer needs.”

The ACCC’s brief is to balance its inquiry and consider that for many Australians, interest payments are an important source of income, while at the same time recognise that deposits play an important role in bank funding (an important consideration given there is currently a focus on the resilience of the banking system).

The inquiry will focus on retail deposits and will not consider accounts held for business purposes, offset and redraw facilities linked to home loans, or pre-paid card facilities.

It will also look at barriers to entry, saying “there are some indications that in the Australian banking sector new entrants pose only a limited competitive constraint. We are interested to understand whether the experience of new entrants indicates that barriers to expansion may be preventing new entrants from growing and achieving sufficient scale to compete.”