While most workers across the Australian banking industry are already pocketing 5 per cent salary rises this year, the Reserve Bank and the Finance Sector Union remain at loggerheads over pay and conditions after six months of sporadic and almost fruitless enterprise talks.

The RBA next week will put a revised three-year pay offer to a staff vote following a decision to disengage from formal negotiations with the union.

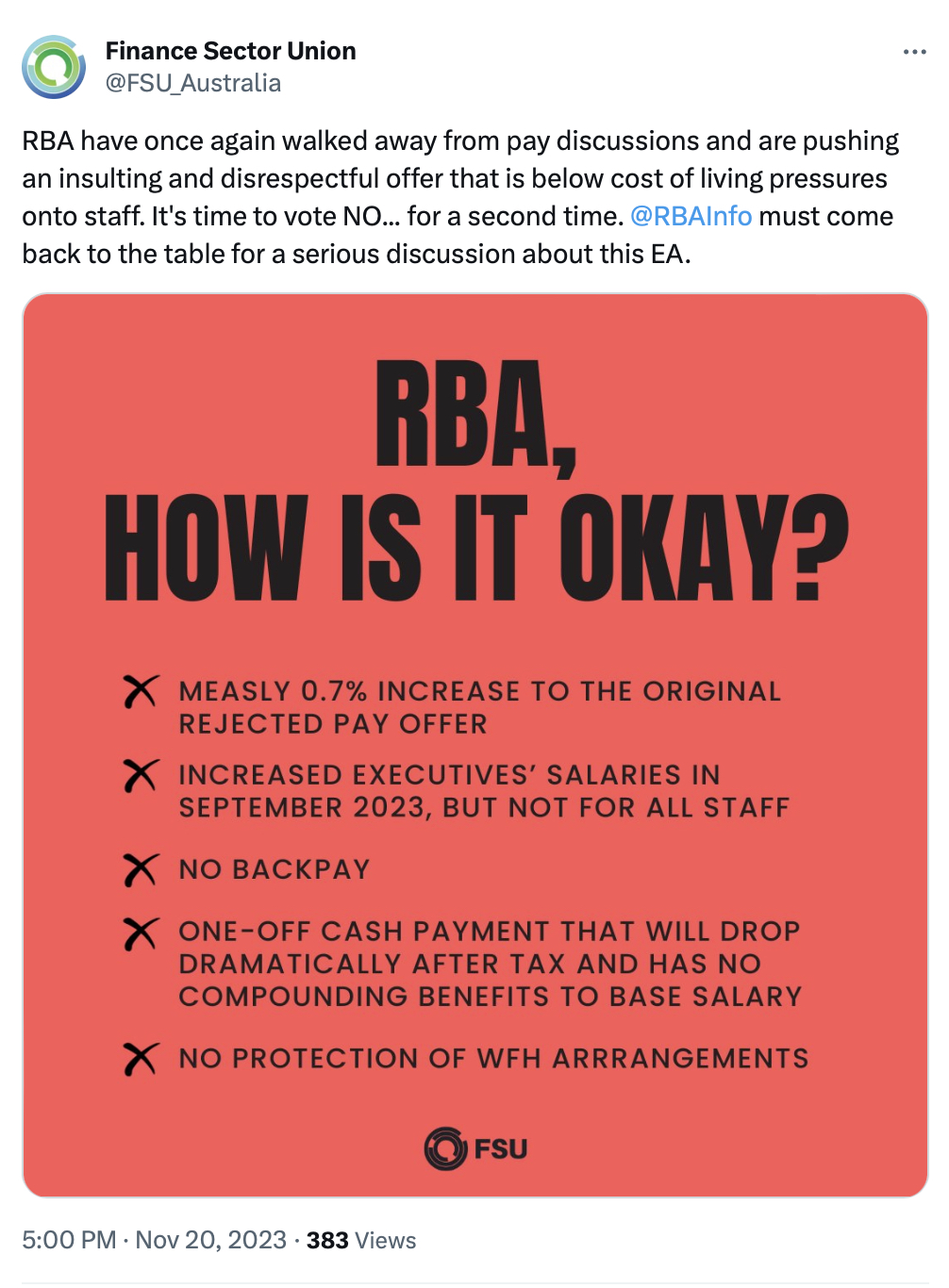

Although the bank has not moved on its 2023 pay rise offer of 4 per cent, it has sweetened pay rises in 2024 and 2025 by a total of 0.7 per cent.

The revised offer would hand RBA employees total pay rises worth 11.2 per cent over three years compared to the 10.5 per cent offer rejected by staff in August.

The RBA has also boosted the pay proposal with a one-off cash payment of A$1000 that is contingent on a majority of eligible staff accepting the offer.

However, the RBA has refused to back-date the wage rise to the start of September when the new agreement was planned to start.

Voting in the second ballot is due to open on 28 November, with the union and the bank now campaigning vigorously to garner support for their respective positions.

The FSU this week intensified its messaging to RBA staff on social media platforms with posts encouraging them to shoot down the “disrespectful” pay offer.

“RBA have once again walked away from pay discussions and are pushing an insulting and disrespectful offer that is below cost of living pressures onto staff,” the union said on X (formerly Twitter).

“It's time to vote NO... for a second time.”

The union is also raising concerns about the bank’s refusal to enshrine work from home rights and some leave entitlements in the enterprise agreement.

While the RBA has developed policies supporting work from home, cultural leave and gender affirmation leave, the union argues such entitlements would be at risk unless they were included in the agreement.

The bank’s hybrid work policy encourages staff to spend at least half their time working from an RBA worksite.

Another sticking point is the escalation of the Reserve Bank’s outsourcing programs in recent years, which has seen the size of its short term contract workforce soar.

Disclosures in the 2022 annual report indicate that more than half of the 285 employees hired in 2022 were recruited on short-term contracts.

In the 12 months to the end of June 2023, the RBA hired 330 new staff and almost half were placed on fixed term contracts.

The bank has acknowledged in recent annual reports that it has faced challenges to attract and retain staff.

Around 13.1 per cent of staff resigned from positions at the bank in 2022, a significant increase on the 7.7 per cent turnover rate of the previous year.

While the RBA stated in its most recent annual report that its turnover rate declined in 2023, it made no specific disclosure about the percentage of staff who resigned their positions.